The Corporate Sustainability Directive (CSRD) is an European Union directive designed to enhance the scope and quality of sustainability reporting by corporations operating within the EU. It mandates the detailed disclosure of a wide range of sustainability-related information. The CSRD replaces the Non-Financial Reporting Directive (NFRD) to meet growing demands for transparency.

Key Changes from NFRD:

| Extended Reporting Requirements | Standardisation | Third-Party Assurance | Digital Reporting |

| Includes more companies. | Ensures comparability of information. | Introduces mandatory assurance for credibility. | Uses digital formats for easier access and analysis. |

The CSRD is part of the broader EU Sustainable Finance Framework, and it works alongside the EU Taxonomy and the Sustainable Finance Disclosure Regulation (SFDR) to achieve EU Green Deal goals.

Key element of CSRD reporting:

Double materiality allows for a dual focus reporting on how company operations impact ESG factors, and how ESG factors affect business operations. Following the CSRD directive, companies must report on Impacts, Risks, and Opportunities (IROs) related to their operations and value chain.

Objectives:

| Transparency and Consistency | Reliable and Comparable Information | Support EU Goals | Foster Sustainable Practices |

| Standardised reporting for easy access and understanding. | Integrates sustainability with financial reports for comprehensive stakeholder insight. | Aligns with the European Green Deal and aims for climate neutrality by 2050. | Encourages integration of sustainability risks and opportunities into business strategies. |

Scope:

| Entities | Geographical and Sectoral Reach | Sustainability Information |

| All large companies, listed SMEs, and non-EU companies with significant EU operations. | Global impact, affecting companies across all sectors with significant EU presence. | Reports on ESG issues, impacts, risks, and opportunities related to business strategies. |

The CSRD applies to all large companies and all companies listed on EU regulated markets, excluding micro-enterprises. The list is estimated to cover approximately 50,000 companies, a

significant increase from the 11,000 under the NFRD.

Companies should prepare for full compliance, building robust systems for data collection and reporting.

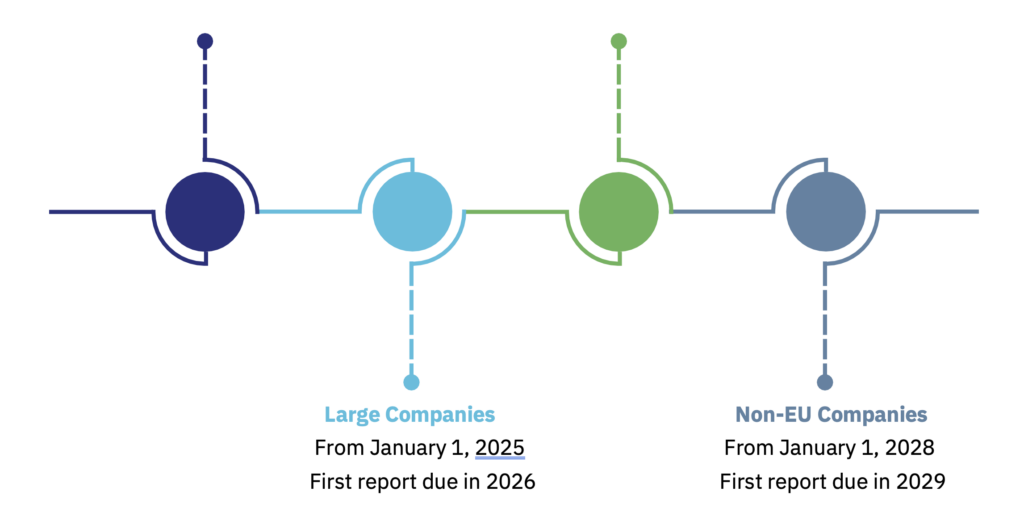

NFRD Companies Listed SMEs

From January 1, 2024 From January 1, 2026

First report due in 2025 First report due in 2027

Optional two-year opt-out with an explanatory statement

Omission of anticipated financial effects from climate and other environmental impacts allowed.

Qualitative disclosures allowed if quantitative disclosures are impracticable.

May omit data on GHG emissions, biodiversity, resource use, and social disclosures in first two reporting years.

Traditional financial statements

Financial implications of sustainability risks and opportunities

Environmental matters: Emissions, waste management, resource conservation

Social concerns: Employee well-being, human rights, community relations

Governance issues: Board diversity, executive remuneration, anti-corruption measures

| Governance | Structures Policies Practices related to sustainability |

| Strategy and Business Model | Sustainability strategy Objectives Alignment with overall business strategy |

| Impacts, Risks, and Opportunities (IROs) | Processes for identifying and assessing material impacts Sustainability risks and opportunities. |

| Metrics and Targets |

Copyright © 2025. All Ireland Sustainability

Webdesign & Development Northern Ireland 2b:creative

Entries have now closed. We would love it if you could join us for our awards evening on the 24th of October at La Mon, Hotel, Belfast!